65 / 120

65 / 120

62

Mega ICBC

-62-

(A)

Credit extensions

Classification of credit assets and internal risk ratings are as follows:

a.

Classification of credit assets

Corporate credit risk is measured by using the borrower’s default probability model with logistic regression analysis in which

financial and non-financial factors are incorporated, which predicts the default probability of borrower within the next year.

Besides, the extent of risk is measured by using credit rating table and taking into account the characteristics and scale of

business. Lending examination and post management are dealt with based on clients’ credit rating. Individual borrowers are

grouped into different risk levels and managed by using application scoring and behavior scoring cards. Back-testing is

conducted on internal models regularly; those models are subject to adjustments when necessary. Clients’ credit ratings are

reviewed annually and subject to adjustments when there is significant change in their credit ratings.

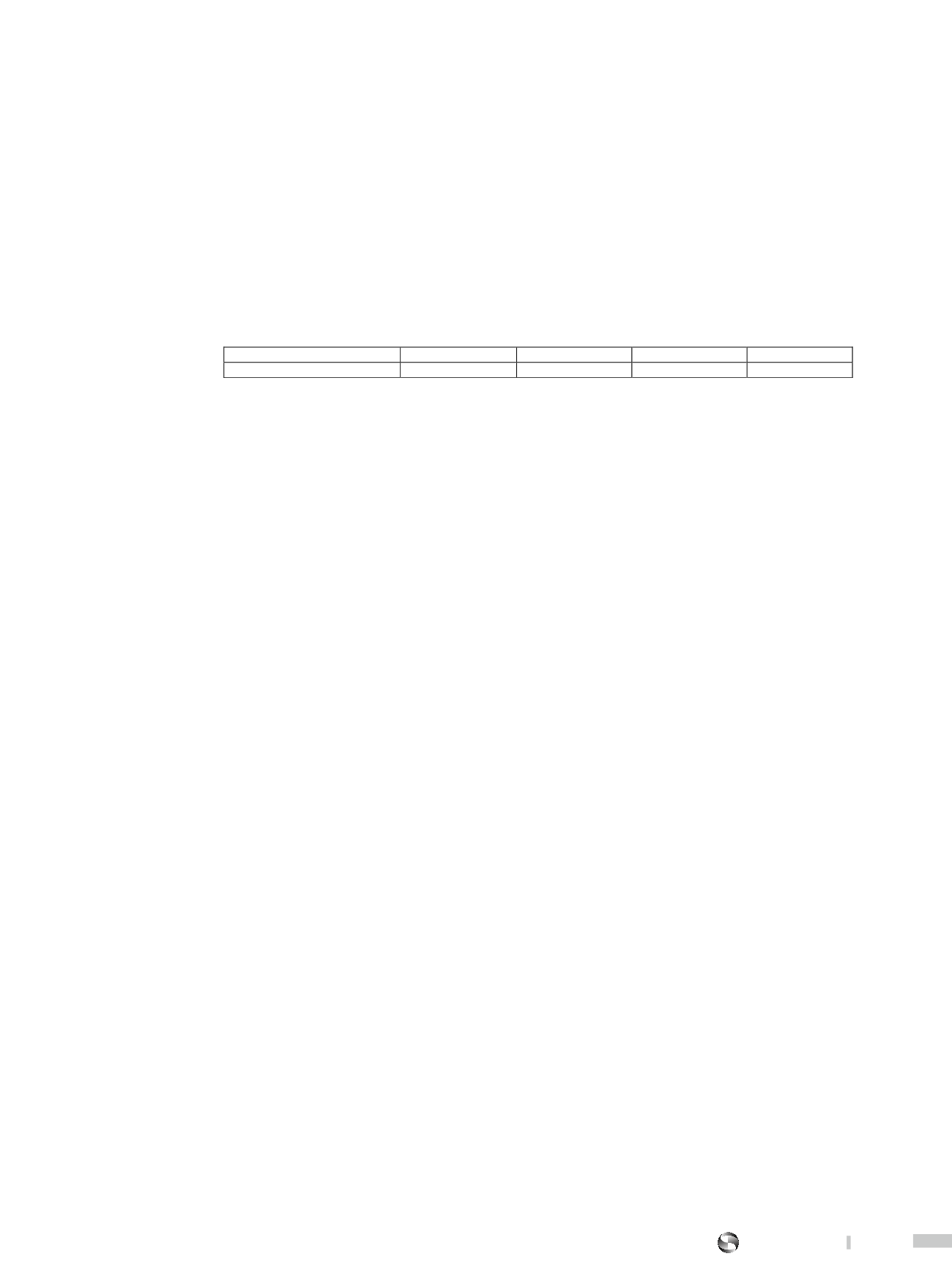

b. Internal risk rating

The internal rating for lending is classified as excellent, satisfactory, fair and weak, and corresponds to the Standard & Poor’s

rating as follows:

Internal risk rating

Excellent

Satisfactory

Fair

Weak

Corresponding to S&P

AAA~BBB-

BB+~ BB-

B+

B and below

(B)

Interbank deposits and call loans

Before trading with other banks, the Bank and its subsidiaries must assess the credit of the counterparty; generally referencing

external rating agencies, assets and scale of equity of the counterparty, and the credit rating of the counterparty’s country of origin

in order to set different transaction limits, as well as periodically examining the stock prices and ratings of the counterparty in order

to monitor the risks of counterparty.

(C)

Bonds and derivative instruments

The limits of bonds purchased by the Bank and its subsidiaries are set by considering the credit rating of bond issuers or guarantors

(ex. S&P, Moody’s, Fitch, Taiwan ratings or Fitch Taiwan), which needs to meet the minimum rating set by the Board of (Managing)

Directors, and country risk at the application, changes in CDS quoted prices and market condition.

The Bank and its subsidiaries have set trading units and overall total risk limit for non-hedging derivative instruments, and use

positive trading contract evaluation and the potential exposure as the basis for calculating credit risk and add the limit to the total

credit risk limit for monitoring.

(D)

Asset quality

The Bank and its subsidiaries have set the minimum requirements and examination procedures for the quality of financial assets of

each type, and controls risk concentration of assets portfolios of each type based on the risk limit of each type. The Bank and its

subsidiaries also monitor the changes in assets quality regularly during the duration of the assets and takes measures to maintain

their quality. According to the policies and regulations, reserve for losses is provided adequately for those assets to actually reflect

and safeguard the value of owners’ equity.

(E)

Impairment of financial assets and provision for reserves

The Bank and its subsidiaries assess at each balance sheet date whether a financial asset is impaired. If there is objective evidence

that an event that occurred after the initial recognition of the asset has an impact on the future cash flows of the financial asset, the

impairment loss on the financial asset should be recognised.

The objective evidence of an impairment loss is as follows:

Significant financial difficulty of the issuer or debtor;

The issuer or debtor has breached the contract;

The Creditor, for economic or legal reasons relating to the borrower’s financial difficulty, granted the borrower a concession;

It becomes probable that the borrower will enter bankruptcy or other financial reorganisation;

The disappearance of an active market for that financial asset because of financial difficulties; or observable data indicating that

there is a measurable decrease in the estimated future cash flows from a group of financial assets since the initial recognition of

those assets, although the decrease cannot yet be identified with the individual financial asset in the group, including:

Adverse changes are in the payment status of borrowers in the group; or adverse changes in national or local economic conditions

that correlate with defaults on the assets in the group.

Financial assets that are not impaired are included in the group of financial assets sharing similar credit risk characteristics for

collective assessment. Financial assets that are assessed individually with impairment recognised need not be included in the

collective assessment.

The amount of the impairment loss is the difference between the financial assets’ book value and the estimated future cash flow

discounted using the original effective interest rate. The present value of estimated future cash flows must reflect the cash flows that

might generate from collaterals less acquisition or selling cost regarding the collateral.

Financial assets through collective assessment are grouped based on similar credit risk characteristics, such as types of assets,

industry and collaterals. Such credit risk characteristics represent the ability of the debtors to pay all the amounts at maturities

according to the contract term, which is related to future cash flows of group of financial assets. The future cash flows of group of

financial assets for collective assessment are estimated based on historical impairment experience, reflecting the change in

observable data for each period, and the estimation of the future cash flows should move in the same direction. The Bank and its

subsidiairies review the assumptions and methods for estimation of the future cash flows regularly.