60 / 120

60 / 120

57

Annual Report 2015

-57-

(35)

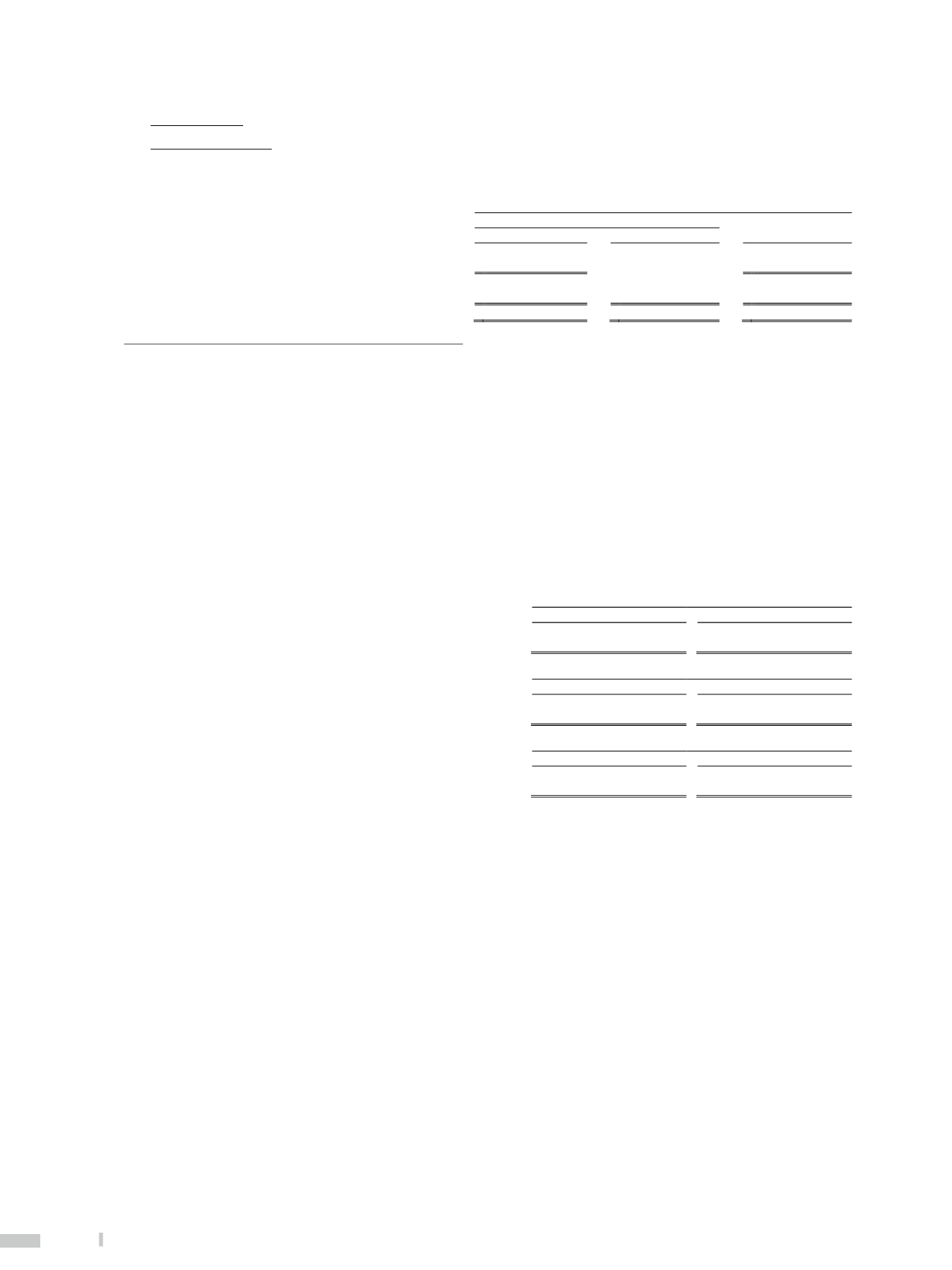

Earnings per share

Basic earnings per share

Basic earnings per share is calculated by dividing the profit attributable to ordinary shareholders of the parent by the weighted-average number

of ordinary shares in issue during the period.

For the years ended December 31,

2015

2014

NT$

US$

NT$

Weighted-average number of shares outstanding common

stock (Unit: Thousands)

7,870,609

7,700,000

Profit attributable to ordinary shareholders of the Bank and its

subsidiaries

$

25,708,445 $

781,697 $

25,990,682

Basic earnings per share (in dollars)

$

3.27 $

0.10 $

3.37

7.

FAIR VALUE INFORMATION OF FINANCIAL INSTRUMENTS

(1)

Overview

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants

at the measurement date. Financial instruments are recorded at fair value upon their initial recognition, where often fair value refers to the

transaction price; for subsequent measurements, other than a portion of financial instruments being measured at amortized cost, fair value is

elected for measurements. The best evidence for fair value is a public quote in an active market. If the market of a financial instrument is not

active, the Bank elects valuation techniques or references Bloomberg or the quotes of counterparties to measure the fair value of the financial

instrument. In addition, through the valuation process, information on the counterparty’s and the Bank’s credit risk is also considered.

(2)

Fair value information of financial instruments

Except for those listed in the table below, the carrying amounts of certain financial instruments held by the Bank and its subsidiaries (such as

cash and cash equivalents, due from Central Bank and call loans to other banks, investments in bills and bonds under resale agreement,

accounts receivable, bills discounted and loans, held-to-maturity financial assets-Central Bank time deposits, due to Central Bank and other

banks, funds borrowed from the Central Bank and other banks, bills and bonds payable under repurchase agreements, accounts payable,

deposits and remittances, financial bonds payable, and other financial liabilities) are approximate to their fair values (please refer to Note

7(4)). The fair value information of financial instruments measured at fair value is provided in Note 7(5).

NT$

Book Value

Fair Value

December 31, 2015

Held-to-maturity financial assets - investments in bonds

$

28,158,540 $

28,111,006

US$

Book Value

Fair Value

December 31, 2015

Held-to-maturity financial assets - investments in bonds

$

856,195 $

854,750

NT$

Book Value

Fair Value

December 31, 2014

Held-to-maturity financial assets - investments in bonds

$

18,595,040 $

18,618,174

The fair values of the above-mentioned held-to-maturity financial assets are classified as Level 1 and Level 2.

(3)

Financial instruments measured at fair value

If the market quotation from the Taiwan Stock Exchange Corporation, brokers, underwriters, Industrial Trade Unions, pricing service agencies

or competent authorities can be frequently obtained on time, and the price represents the actual and frequent transactions at arm’s length, then

a financial instrument is deemed to have an active market. If the above condition cannot be met, the market is deemed inactive. In general,

significant price variance between the purchase price and selling price, significantly increasing price variance or extremely low trading volume

are all indicators of an inactive market.

If the quoted market price of a financial instrument is available in an active market, the quoted price is the fair value, usually the fair value is

measured using the market price, interest rate, foreign exchange central parity rate shown in Reuters quotation system, partially using the

quoted prices from Bloomberg, OTC, and the basis for valuation is maintained consistently. If there is no quoted market price for reference,

a valuation technique or quoted price offer by the counterparties will be adopted to measure the fair value. Fair value measured by a valuation

technique is usually estimated by reference to the fair values of other financial instruments with similar terms and characteristics, or by using

cash flows discounting method, or using model calculation based on the market information (such as yield rate curves from OTC, average

interest rate of commercial papers from Reuters) available on the balance sheet date.

When assessing non-standardized financial instruments with lower complexity, derivative financial instruments such as interest rate swap

contracts, foreign exchange swap contracts, options, the Bank and its subsidiaries use valuation techniques and models which are extensively

used by the market to estimate their fair value. The parameters used in the valuation model for these kinds of financial instruments usually

use the observable information as the input.

For more complicated financial instruments, such as debt instruments with embedded derivative instruments or securitization products, the

Bank and its subsidiaries develop its own valuation models to estimate fair value by reference to the valuation techniques and methods which

are extensively used by the same trade. Parts of parameters used in these valuation models are not observable from the market; they must

be estimated by using some assumptions.