63 / 120

63 / 120

60

Mega ICBC

-60-

C.

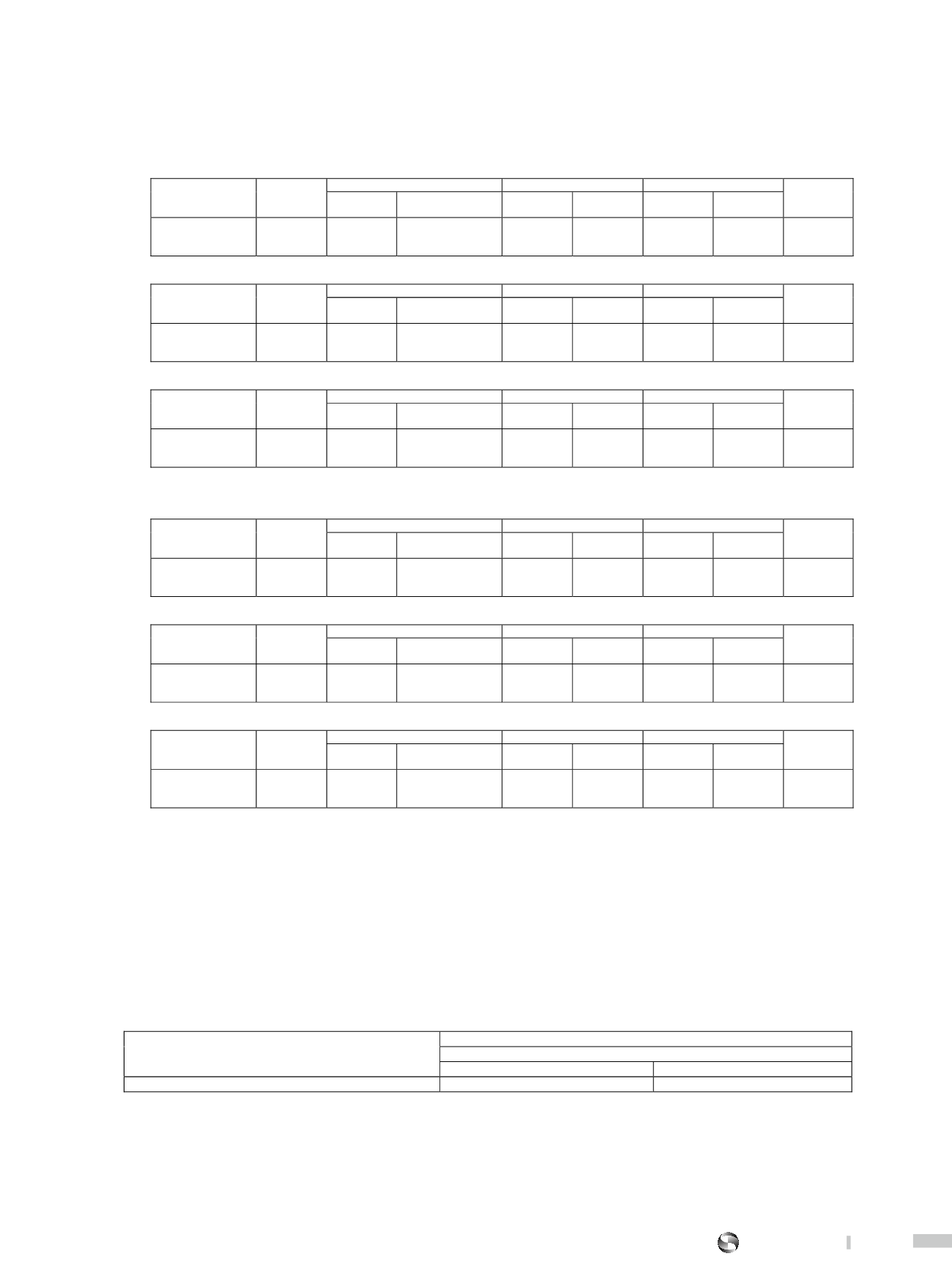

Movements of financial instruments classified into Level 3 of fair value are as follows:

(A)

Movements of financial assets classified into Level 3 of fair value are as follows:

For the year ended December 31, 2015

(In NT Thousand Dollars)

Items

Beginning

balance

Gain and loss on valuation

Addition

Reduction

Ending balance

Gain and loss Other comprehensive

income

Purchased

or issued

Transferred

to Level 3

Sold, disposed

or settled

Transferred

from Level 3

Financial assets at fair

value through profit

or loss

$

214,281 $

106,135 $

- $

14,514 $

- ( $

472 ) ($ 334,458) $

-

For the year ended December 31, 2015

(In US Thousand Dollars)

Items

Beginning

balance

Gain and loss on valuation

Addition

Reduction

Ending balance

Gain and loss Other comprehensive

income

Purchased

or issued

Transferred

to Level 3

Sold, disposed

or settled

Transferred

from Level 3

Financial assets at fair

value through profit

or loss

$

6,515 $

3,227 $

- $

441 $

- ( $

14 ) ($

10,169 ) $

-

For the year ended December 31, 2014

(In NT Thousand Dollars)

Items

Beginning

balance

Gain and loss on valuation

Addition

Reduction

Ending balance

Gain and loss Other comprehensive

income

Purchased

or issued

Transferred

to Level 3

Sold, disposed

or settled

Transferred

from Level 3

Financial assets at fair

value through profit

or loss

$

700,069 ($

206,346) $

- $

376,055 $

- ( $ 242,019 ) ($ 413,478 ) $

214,281

(B)

Movements of financial liabilities classified into Level 3 of fair value are as follows:

For the year ended December 31, 2015

(In NT Thousand Dollars)

Items

Beginning

balance

Gain and loss on valuation

Addition

Reduction

Ending balance

Gain and loss Other comprehensive

income

Purchased

or issued

Transferred

to Level 3

Sold, disposed

or settled

Transferred

from Level 3

Financial liabilities at

fair value through

profit or loss

($

214,281) ($

106,135) $

- ($

14,514) $

- $

472 $

334,458 $

-

For the year ended December 31, 2015

(In US Thousand Dollars)

Items

Beginning

balance

Gain and loss on valuation

Addition

Reduction

Ending balance

Gain and loss Other comprehensive

income

Purchased

or issued

Transferred

to Level 3

Sold, disposed

or settled

Transferred

from Level 3

Financial liabilities at

fair value through

profit or loss

($

6,515) ($

3,227) $

- ($

441) $

- $

4 $

10,169 $

-

For the year ended December 31, 2014

(In NT Thousand Dollars)

Items

Beginning

balance

Gain and loss on valuation

Addition

Reduction

Ending balance

Gain and loss Other comprehensive

income

Purchased

or issued

Transferred

to Level 3

Sold, disposed

or settled

Transferred

from Level 3

Financial liabilities at

fair value through

profit or loss

($ 1,166,222) $

210,911 $

- ($

617,779) $

- $

449,66 $

909,163 ($ 214,281 )

Due to the adoption of observable inputs rather than quoted price from counterparties, derivative financial instruments were transferred from

level 3 to level 2.

D.

Transfer between Level 1 and Level 2

The Bank’s held 103-13 and 103-15 Category A Central Government Construction Bonds at December 31, 2015 had an amount of NT$105,180

thousand and NT$153,912 thousand, respectively. For the current period they were not indicative active bonds, thus they were transferred from

Level 1 to Level 2.

E.

Fair value measurement to Level 3, and the sensitivity analysis of the substitutable appropriate assumption made on fair value.

The fair value measurement that the Bank and its subsidiaries made to the financial instruments is deemed reasonable; however, different valuation

models or inputs could results in different valuation results. Specifically, if the valuation input of financial instrument classified in Level 3 moves

upward or downward by 10%, the effects on gain and loss in the period or the effects on other comprehensive income are as follows:

The Bank and its subsidiaries did not hold any Level 3 financial instruments at December 31, 2015

December 31, 2014

Effect of changes in fair value in the current profit and loss

NT$

Favorable change

Unfarorable change

Derivative financial assets and liabilities

$

-

$

-

Favorable and unfavorable movements of the Bank and its subsidiaries refer to the fluctuation of fair value, and the fair value is calculated according

to unobservable parameters to different extent. If the fair value of a financial instrument is affected by one or more inputs, the correlation and

variance of input are not put into consideration in the above table.