82 / 120

82 / 120

79

Annual Report 2015

-79-

(B)

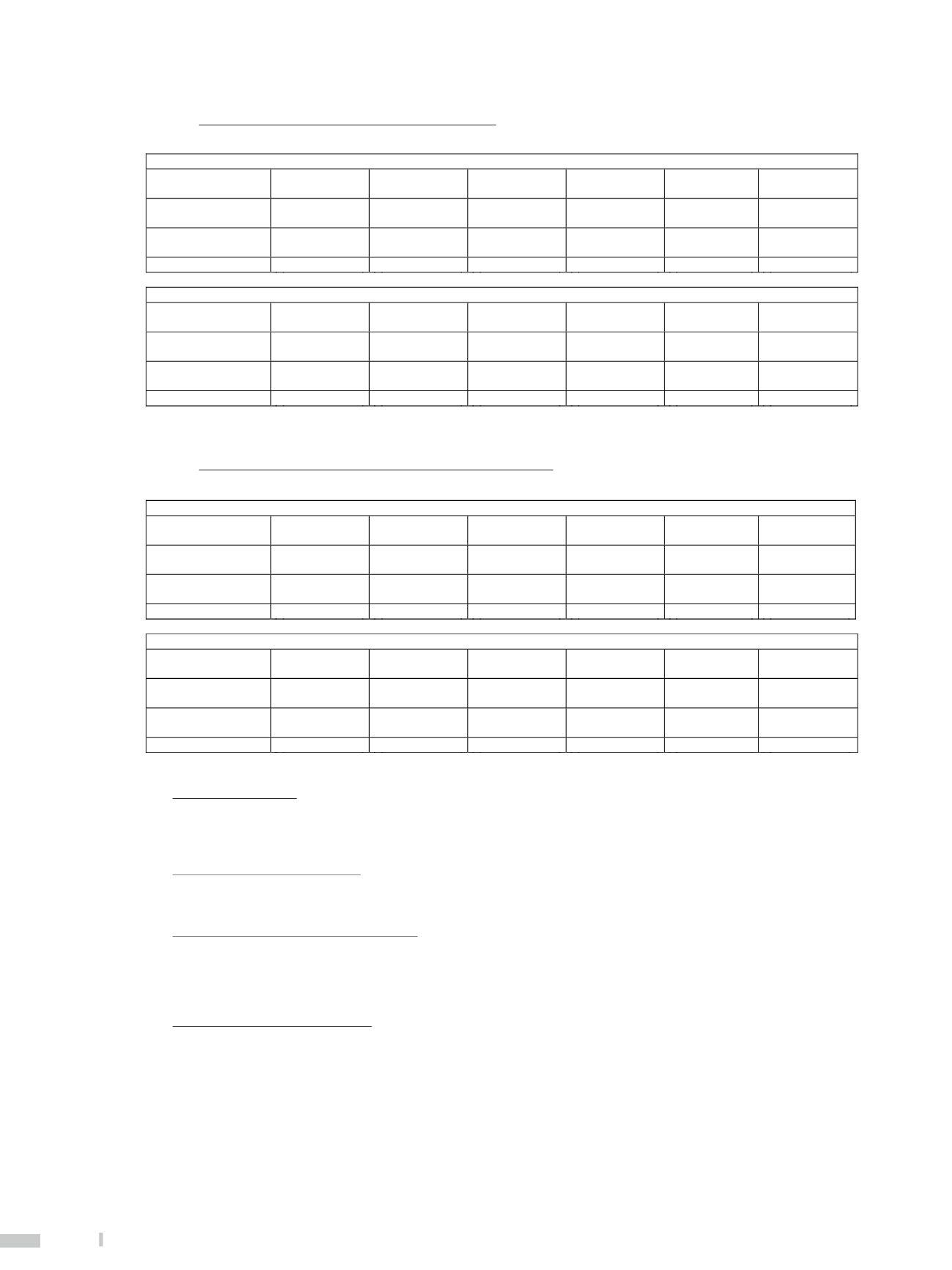

Maturity analysis of USD financial instruments of the Bank

UNIT: In US Thousand Dollars

December 31, 2015

Total

0-30 days

31-90 days

91-180 days

181 days–

1 year

Over 1 year

Primary funds inflow

upon maturity

$ 49,192,216 $

19,824,266 $ 6,928,530 $ 4,372,053 $

3,886,530 $

14,180,837

Primary funds outflow

upon maturity

65,418,953

23,744,666

9,451,321

6,520,937

8,066,411

17,635,618

Gap

($ 16,226,737 ) ($

3,920,400 ) ($ 2,522,791 ) ($ 2,148,884 ) ($

4,179,881 ) ($

3,454,781 )

December 31, 2014

Total

0-30 days

31-90 days

91-180 days

181 days–

1 year

Over 1 year

Primary funds inflow

upon maturity

$ 46,951,288 $

17,589,733 $ 6,585,580 $ 4,185,118 $

5,281,519 $

13,309,338

Primary funds outflow

upon maturity

67,917,707

28,432,372

7,282,055

7,072,663

8,945,456

16,185,161

Gap

($ 20,966,419 ) ($

10,842,639 ) ($

696,475 ) ($ 2,887,545 ) ($

3,663,937 ) ($

2,875,823 )

Note 1: The funds denominated in US dollars means the amount of all US dollars of the Bank.

Note 2: If overseas assets exceed 10% of total assets, supplementary information shall be disclosed.

(C)

Maturity analysis of USD financial instruments of the foreign branches

UNIT

:

In US Thousand Dollars

December 31, 2015

Total

0-30 days

31-90 days

91-180 days

181 days–

1 year

Over 1 year

Primary funds inflow

upon maturity

$ 18,389,498 $

9,879,840 $ 1,940,168 $

872,192 $

883,489 $

4,813,809

Primary funds outflow

upon maturity

21,068,444

12,305,964

1,083,854

942,448

1,188,771

5,547,407

Gap

($ 2,678,946 ) ($

2,426,124 ) $

856,314 ($

70,256 ) ($

305,282 ) ($

733,598 )

December 31, 2014

Total

0-30 days

31-90 days

91-180 days

181 days–

1 year

Over 1 year

Primary funds inflow

upon maturity

$ 17,994,406 $

10,605,599 $ 1,793,273 $

750,828 $

870,644 $

3,974,062

Primary funds outflow

upon maturity

20,208,347

12,397,830

1,644,153

1,630,766

375,053

4,160,545

Gap

($ 2,213,941 ) ($

1,792,231 ) $

149,120 ($

879,938 ) $

495,591 ($

186,483 )

(5)

Market risk

A.

Definition of market risk

Market risk refers the potential losses of the Bank’s and its subsidiaries’ on-balance-sheet and off-balance-sheet positions due to the Bank

and its subsidiaries enduring fluctuations of market prices (for example: fluctuations of market interest, exchange rates, stock prices and

price of products).

B.

Objective of market risk management

The objective of the Bank’s and its subsidiaries’ market risk management is to confine risks within a tolerable scope to avoid the

fluctuations of financial product prices impacting furture returns and the values of assets and liabilities.

C.

Market risk management policies and procedures

The Board of (Managing) Directors decided the risk tolerant limits, position limits, and loss limits. Market risk management comprises

trading book control and banking book control. Trading book operation mainly pertains to the positions held by bills and securities firms

due to market making. Policies for financial instrument trading of bank are based on back-to-back operation principle. Banking book is

based on held-to-maturity principle and adopts hedging measures.

D.

Procedures for market risk management

(A)

The Bank’s objectives of market risk management are respectively proposed by The Treasury Department and The Financial Risk

Management Center, and then Risk Control Department summarizes and reports these objectives to Risk Management Committee

of Mega Financial Holdings and the Bank’s Board of Directors for assessment.

(B)

Financial Risk Management Center not only prepares statement of market risk position and profit and loss of various financial

instruments but regularly compiles securities investment performance evaluation and reports to the Board of (Managing) Directors

for the Board’s knowledge of the Bank’s risk control over securities investment. Risk Management Department summarizes and