86 / 120

86 / 120

83

Annual Report 2015

-83-

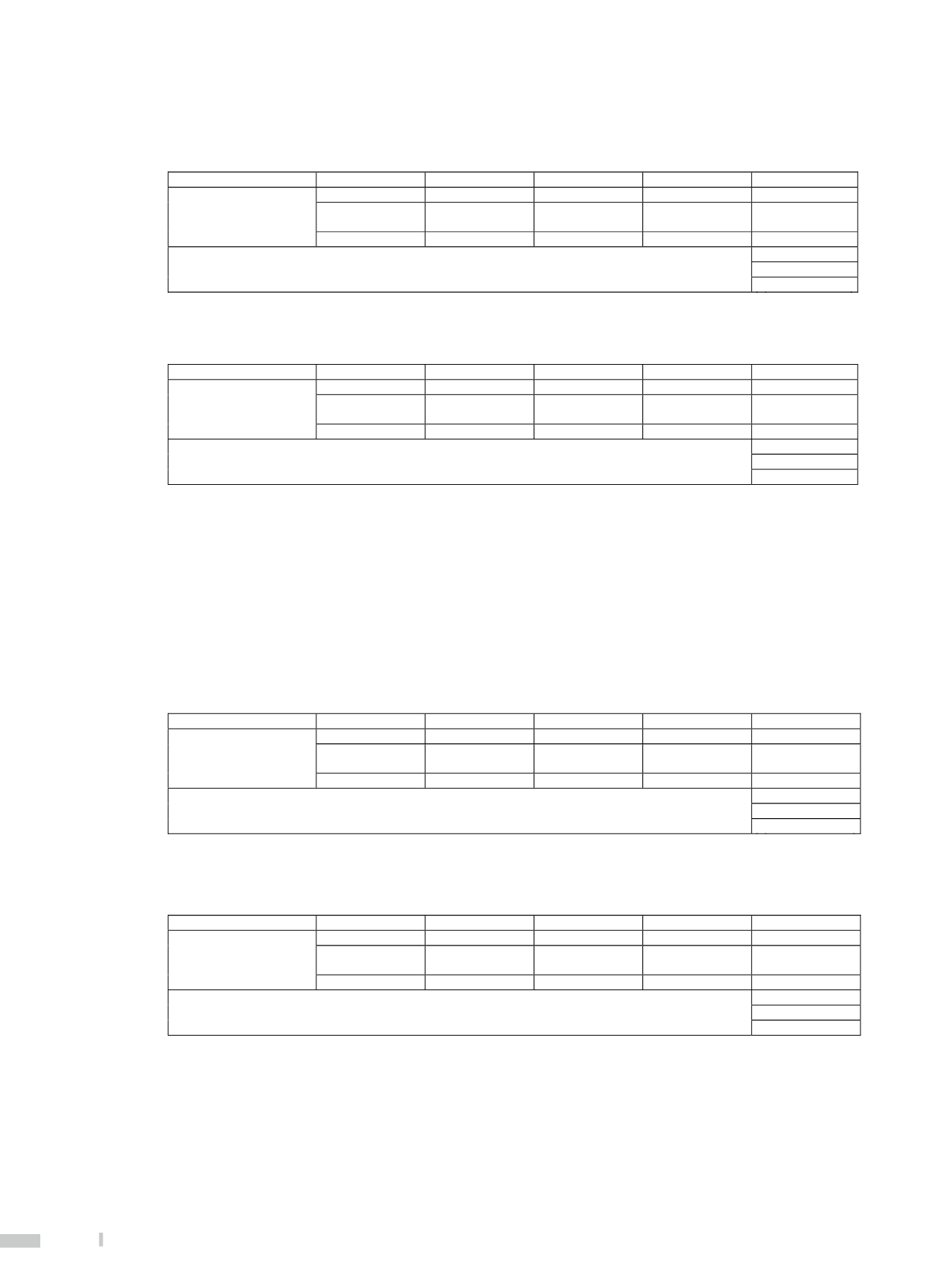

Interest rate sensitivity analysis on assets and liabilities (NT Dollars)

December 31, 2015

UNIT

:

In US Thousand Dollars, %

1-90 days

91-180 days

181 days to 1 year

Over 1 year

Total

Interest rate sensitive assets $

15,697,725 $ 25,177,781 $

223,924 $

1,343,818 $

42,443,248

Interest rate sensitive

liabilities

14,430,011

18,742,449

2,676,896

1,358,691

37,208,047

Interest rate sensitive gap

$

1,267,714 $

6,435,332 ( $

2,452,972 ) ( $

14,873 ) $

5,235,201

Net worth

$

7,285,095

Ratio of interest rate sensitive assets to interest rate sensitive liabilities

114.07%

Ratio of interest rate sensitivity gap to net worth

71.86%

Interest rate sensitivity analysis on assets and liabilities (NT Dollars)

December 31, 2014

UNIT

:

In NT Thousand Dollars, %

1-90 days

91-180 days

181 days to 1 year

Over 1 year

Total

Interest rate sensitive assets $

517,544,862 $ 793,633,242 $

5,458,866 $ 21,875,492 $ 1,338,512,462

Interest rate sensitive

liabilities

531,933,123

577,848,161

40,867,077

41,273,642 1,191,922,003

Interest rate sensitive gap

( $

14,388,261 ) $ 215,785,081 ( $

35,408,211 ) ( $ 19,398,150 ) $

146,590,459

Net worth

$

201,084,879

Ratio of interest rate sensitive assets to interest rate sensitive liabilities

112.30%

Ratio of interest rate sensitivity gap to net worth

72.90%

Notes

:

1. The above amounts included only New Taiwan dollar amounts by the onshore branches of the Bank (i.e. excluding foreign

currency).

2. Interest rate sensitive assets and liabilities refer to the interest-earning assets and interest-bearing liabilities of which the income

or costs are affected by the fluctuations in interest rates.

3. Interest rate sensitivity gap = Interest rate sensitive assets – Interest rate sensitive liabilities

4. Ratio of interest rate sensitive assets to interest rate sensitive liabilities = Interest rate sensitive assets ÷ Interest rate sensitive

liabilities (referring to the current interest rate sensitive assets and liabilities denominated in New Taiwan dollars)

Interest rate sensitivity analysis on assets and liabilities (US Dollars)

December 31, 2015

UNIT

:

In US Thousand Dollars, %

1-90 days

91-180 days

181 days to 1 year

Over 1 year

Total

Interest rate sensitive assets $

32,285,909 $

1,802,050 $

393,155 $

366,323 $

34,847,437

Interest rate sensitive

liabilities

33,693,738

1,497,285

1,141,957

535,953

36,868,933

Interest rate sensitive gap

( $

1,407,829 ) $

304,765 ( $

748,802 ) ( $

169,630 ) ( $

2,021,496 )

Net worth

$

544,916

Ratio of interest rate sensitive assets to interest rate sensitive liabilities

94.52%

Ratio of interest rate sensitivity gap to net worth

-370.97%

Interest rate sensitivity analysis on assets and liabilities (US Dollars)

December 31, 2014

UNIT

:

In US Thousand Dollars, %

1-90 days

91-180 days

181 days to 1 year

Over 1 year

Total

Interest rate sensitive assets $

31,787,537 $

989,720 $

535,738 $

632,660 $

33,945,655

Interest rate sensitive

liabilities

32,523,628

1,140,004

1,000,605

502,402

35,166,639

Interest rate sensitive gap

( $

736,091 ) ( $

150,284 ) ( $

464,867 ) $

130,258 ( $

1,220,984 )

Net worth

$

626,391

Ratio of interest rate sensitive assets to interest rate sensitive liabilities

96.53%

Ratio of interest rate sensitivity gap to net worth

-194.92%

Note

:

1. The above amounts included only US dollars denominated assets and liabilities of head office, domestic and foreign branches,

and the OBU branch. Contingent assets and liabilities are excluded.

2. Interest rate sensitivity gap = Interest rate sensitive assets – Interest rate sensitive liabilities.

3. Ratio of interest rate sensitive assets to interest rate sensitive liabilities = Interest rate sensitive assets ÷ Interest rate sensitive

liabilities (referring to the current interest rate sensitive assets and liabilities denominated in US dollars).