88 / 120

88 / 120

85

Annual Report 2015

-85-

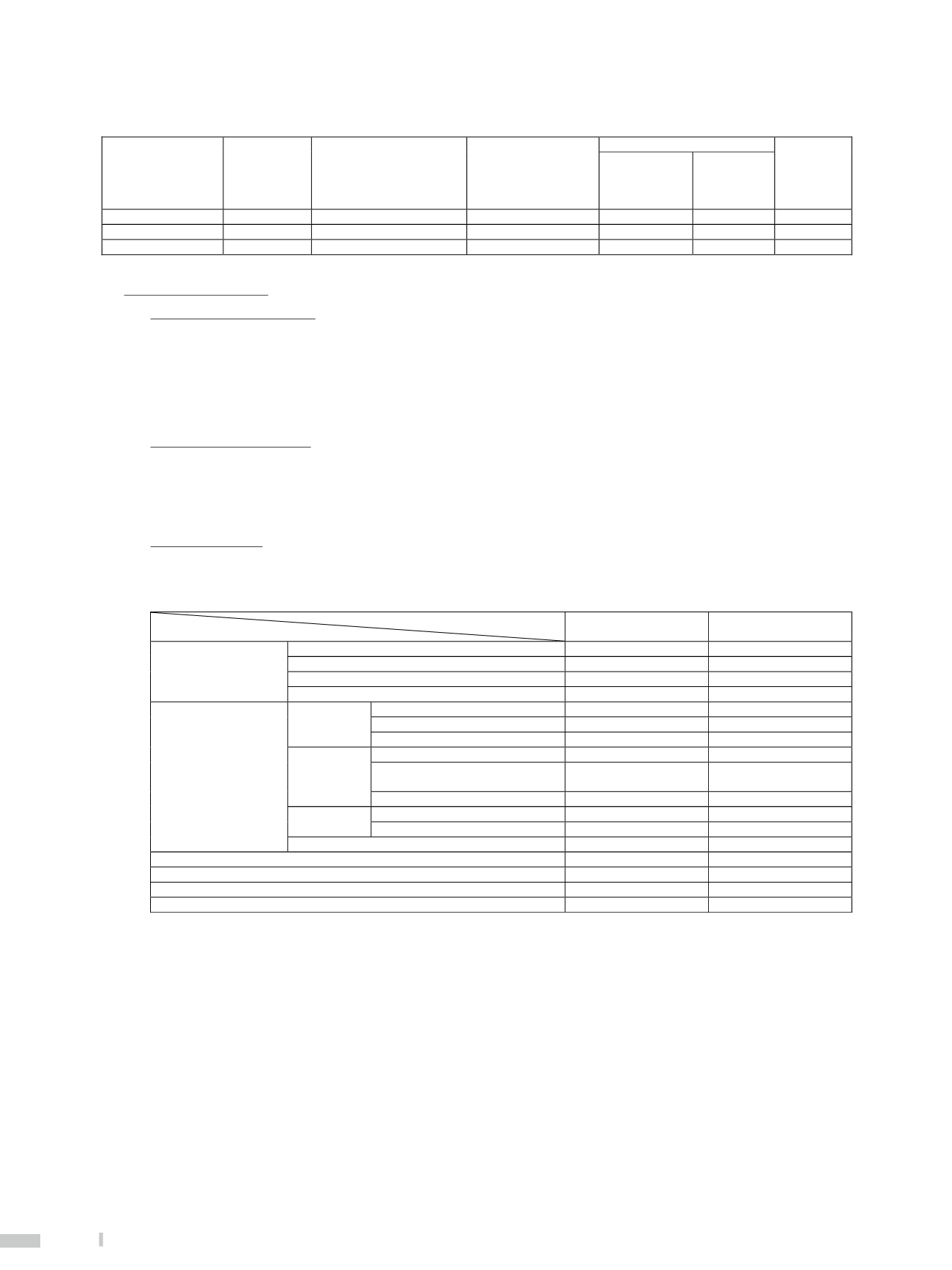

Financial liabilities that are offset, or can be settled under agreements of net settlement master netting arrangements or similar arrangements

Description

Gross amounts

of recognised

financial

liabilities

(a)

Gross amounts of recognised

financial assets offset in the

balance sheet

(b)

Net amounts of financial

liabilities presented in

the balance sheet

(c)=(a)-(b)

Not offset in the balance sheet(d)

Net amount

(e)=(c)-(d)

Financial

instruments

(Note)

Cash collateral

received

Derivative instruments $

7,425,472 $

- $

7,425,472 $

649,138 $

44,464 $ 6,731,870

Repurchase agreement

49,444,677

-

49,444,677

49,444,677

-

-

Total

$

56,870,149 $

- $

56,870,149 $

50,093,815 $

44,464 $ 6,731,870

(Note) Including net settlement master netting arrangements and non-cash collaterals.

9.

CAPITAL MANAGEMENT

(1)

Objective of capital management

A.

The Bank and its subsidiaries’ qualifying self-owned capital should meet the regulatory requirements and meet the minimum regulated

capital adequacy ratio. This is the basic objective of capital management of the Bank and its subsidiaries. The calculation and provision

of qualifying self-owned capital and regulated capital shall follow the regulations of the competent authority.

B. In order to have adequate capital to take various risks, the Bank and its subsidiaries shall assess the required capital with consideration of

the risk portfolio it faces and the risk characteristics, and manages risk through capital allocation to realize optimum utilization of capital

allocation.

(2)

Capital management procedures

A. Following the “Regulations Governing the Capital Adequacy Ratio of Banks” of the Financial Supervisory Commission, the Bank

calculates capital adequacy ratio on a consolidated basis and reports this information regularly.

B. The calculation of capital adequacy ratio of subsidiaries shall follow the regulations of regulatory authorities; if without regulations,

capital adequacy ratio is computed as net of qualifying self-own capital divided by regulated capital.

(3)

Capital adequacy ratio

Capital adequacy shown in the following table was calculated in accordance with “Regulations Governing the Capital Adequacy Ratio of

Banks” effective on December 31, 2015 and 2014.

UNIT

:

In NT Thousand Dollars, %

Annual

Items

December 31, 2015

December 31, 2014

Self-owned capital

Capital of Common equity

$

244,583,282 $

207,734,290

Other Tier 1 Capital

-

-

Tier 2 Capital, net

44,734,116

45,401,452

Self-owned capital, net

289,317,398

253,135,742

Total risk -weighted assets

(Note 1)

Credit risk

Standardized Approach

2,033,605,160

1,983,041,002

Internal Ratings-Based Approach

-

-

Asset securitization

1,375,313

4,171,285

Operation risk

Basic Indicator Approach

89,086,413

85,933,263

Standardized Approach / Alternative

Standardized Approach

-

-

Advanced Measurement Approaches

-

-

Market risk

Standardized Approach

46,141,363

45,428,813

Internal Models Approach

-

-

Total risk-weighted assets

2,170,208,249

2,118,574,363

Capital adequacy ratio (Note 2)

13.33%

11.95%

Total risk assets based Capital of Common equity, net Ratio

11.27%

9.81%

Total risk assets based Tier 1 Capital, net Ratio

11.27%

9.81%

Leverage ratio

7.02%

4.17%

Note 1: The self-owned capital, risk-weighted assets and exposures amount in the table above should be filled in accordance with “Regulations

Governing the Capital Adequacy Ratio of Banks” and “calculation method and table of self-owned capital and risk-weighted assets”.

Note 2: Current and prior year's capital adequacy ratio should be disclosed in the annual reports. In addition to current and prior year's capital adequacy,

capital adequacy ratio at the end of prior year should be disclosed in the semi-annual reports.

Note 3: The relevant formulas are as follows:

1. Self-owned capital = Tier 1 Capital of Common equity, net

+

Other Tier 1 Capital, net

+

Tier 2 Capital, net

2. Total risk-weighted assets = credit risk-weighted assets + (operation risk + market risk) * 12.5

3. Capital adequacy ratio = Self-owned capital / Total risk-weighted assets

4. Total risk assets based Tier 1 Capital of Common equity, net Ratio

=

Tier 1 Capital of Common equity, net / Total risk-weighted assets

5. Total risk assets based Tier 1 Capital, net Ratio

=

(Tier 1 Capital of Common equity, net + Other Tier 1 Capital, net) / Total risk-weighted

assets

6. Gearing ratio = Tier 1 capital/ exposures amount

Note 4: For 1st quarter and 3rd quarter financial reports, the table of capital adequacy ratio is not required to be disclosed.