74 / 120

74 / 120

71

Annual Report 2015

-71-

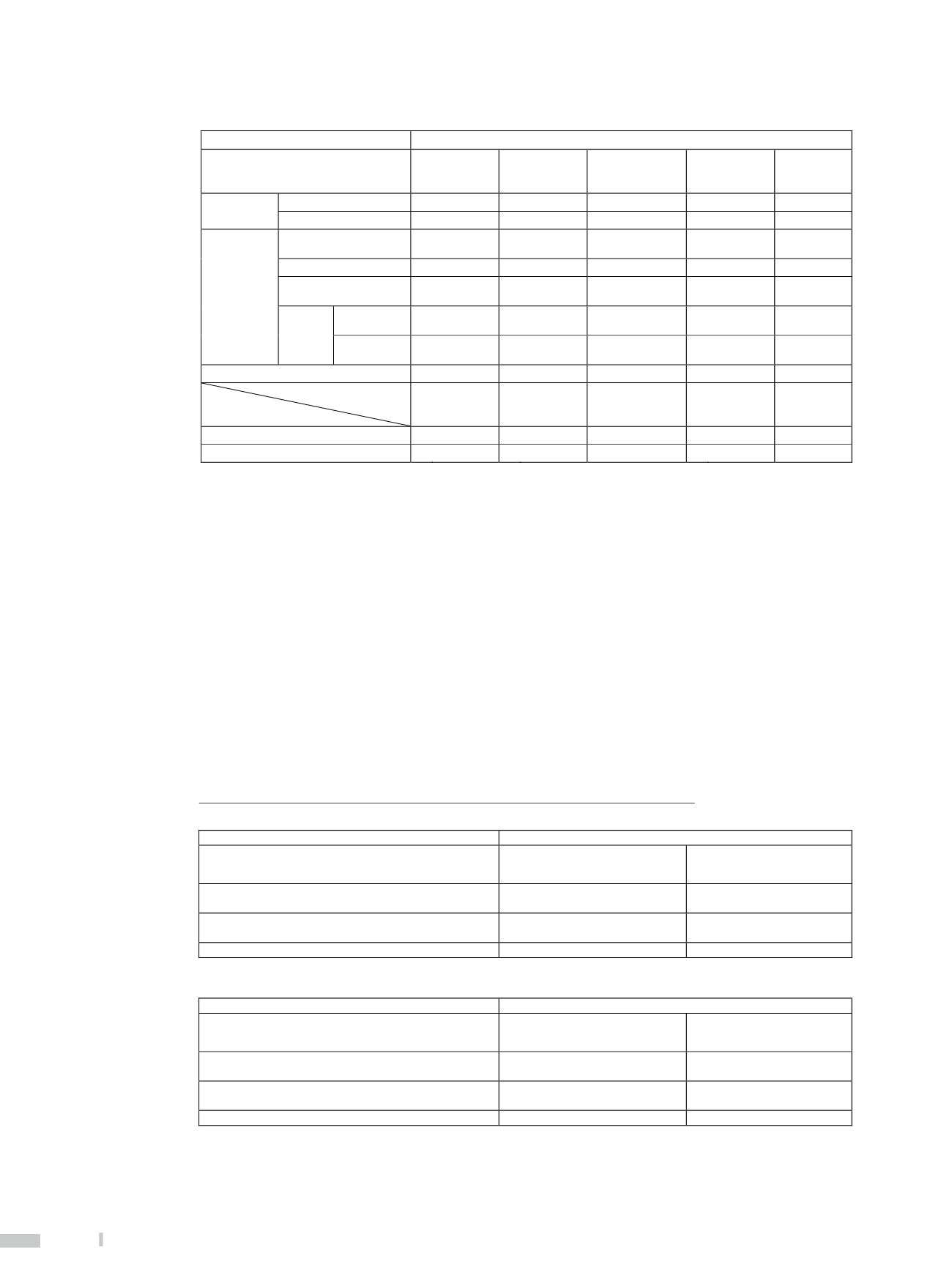

Unit: In NT Thousand Dollars, %

Month/Year

December 31, 2014

Business/Items

Amount of

non-performing

loans (Note 1) Gross loans

Non-performing

loan ratio

(Note 2)

Allowance

for doubtful

accounts

Coverage

ratio (Note 3)

Corporate

Banking

Secured loans

$

448,348 $ 617,988,986

0.07% $

8,068,491

1,799.60%

Unsecured loans

386,045

751,118,032

0.05%

9,650,444

2,499.82%

Consumer

banking

Residential mortgage

loans (Note 4)

359,072

289,753,117

0.12%

3,147,343

876.52%

Cash card services

-

-

-

-

-

Small amount of credit

loans (Note 5)

749

11,115,192

0.01%

118,846

15,867.29%

Others

(Note 6)

Secured

loans

52,840

85,635,206

0.06%

931,650

1,763.15%

Unsecured

loans

-

303,770

-

3,258

-

Gross loan business

$

1,247,054 $

1,755,914,303

0.07% $

21,920,032

1,757.75%

Amount of

overdue

accounts

Balance of

accounts

receivable

Overdue

account ratio

Allowance

for doubtful

accounts

Coverage

ratio

Credit card services

$

7,592

4,300,701

0.18% $

65,063

856.99%

Without recourse factoring (Note 7)

$

4,351 $

46,390,766

0.01% $

695,914

15,994.35%

Notes:

1.

The amount recognised as non-performing loans is in accordance with the “Regulation Governing the Procedures for Banking

Institutions to Evaluate Assets and Deal with Non-performing/Non-accrual Loans”. The amount included in overdue accounts

for credit cards is in accordance with the Financial-Supervisory-Banks (4) Letter No.0944000378 dated July 6, 2005.

2.

Non-performing loan ratio = non-performing loans/gross loans. Overdue account ratio for credit cards=overdue

accounts/balance of accounts receivable.

3.

Coverage ratio for loans = allowance for doubtful accounts of loans/non-performing loans. Coverage ratio for accounts

receivable of credit cards = allowance for doubtful accounts for accounts receivable of credit cards/overdue accounts.

4.

For residential mortgage loans, the borrower provides his/her (or spouses or minor) house as collateral in full and mortgages it

to the financial institution for the purpose of obtaining funds to purchase or add improvements to a house.

5.

Small amount of credit loans apply to the norms of the Financial-Supervisory-Banks (4) Letter No. 09440010950 dated

December 19, 2005, excluding credit card and cash card services.

6.

Other consumer banking is specified as secured or unsecured consumer loans other than residential mortgage loan, cash card

services and small amount of credit loans, and excluding credit card services.

7.

Pursuant to the Financial-Supervisory-Banks (5) Letter No. 094000494 dated July 19, 2005, the amount of without recourse

factoring will be recognised as overdue accounts within three months after the factor or insurance company resolves not to

compensate the loss.

(B)

Non-performing loans and overdue receivables exempted from reporting to the competent authority

Unit: In NT Thousand dollars

December 31, 2015

Total amount of non-performing loans

exempted from reporting to the competent

authority

Total amount of overdue receivables

exempted from reporting to the

competent authority

Performing amounts exempted from reporting to the

competent authority as debt negotiation (Note 1)

$

16 $

-

Performing amounts in accordance with debt liquidation

program and restructuring program (Note 2)

402

3,383

$

418 $

3,383

Unit: In US Thousand dollars

December 31, 2015

Total amount of non-performing loans

exempted from reporting to the competent

authority

Total amount of overdue receivables

exempted from reporting to the

competent authority

Performing amounts exempted from reporting to the

competent authority as debt negotiation (Note 1)

$

- $

-

Performing amounts in accordance with debt liquidation

program and restructuring program (Note 2)

12

103

$

12 $

103